The Fed Won't Get 7 Rate Hikes

Mar 14, 2022It's all coming to a head, the three most important things in markets right now are about to collide. This week ahead should be as wild of a week as we've had in memory.

First, The much anticipated FOMC rate hike announcement and press conference is finally upon us, Thursday afternoon.

The big question is how will the Federal Reserve deal with 7.9% inflation in the US.

A 25 basis point rate hike is priced in the Fed Funds Futures already, which is down from the 50 basis point rate hike expected before Russia invaded Ukraine. A 25 basis point rate hike most likely won't be able to slow the rate of change of inflation.

And to be clear, we all know that the CPI (Consumer Price Index) is a magic formula that doesn't seem to reflect the reality of most people.

For example, here in the Phoenix Metro area, the price of housing (about 1/3 of normal household budget) looks like this:

- Monthly Average Sales Price per Sq. Ft.: $284.55 versus $231.11 last year – up 23.1% – and up 3.6% from $274.70 last month

- Monthly Median Sales Price: $445,000 versus $349,000 last year – up 27.5% – and up 2.7% from $433,500 last month

(Source Metro Realty AZ https://metrorealtyaz.com/arizona-real-estate-market-this-month/)

Gasoline prices on average in the United States right now are $4.196 up from $2.941 just one year ago, that's a 42% increase in one year. (source YCharts https://ycharts.com/indicators/us_gas_price)

Since 1990, and 1980 the way CPI has been tracked has changed, which is good because the cost of a TV or Computer in the 1990's is so much more than what a computer costs today.

On an inflation adjusted basis a Pentium III Desktop Computer would set you back $4.076, in 1999. Today you can get a desktop from Best Buy for $500.

So yeah, things have changed in price over the years, as have things that consumers purchase. Sure many people had exercise bikes in our house in 1999, but Pelaton wasn't a thing.

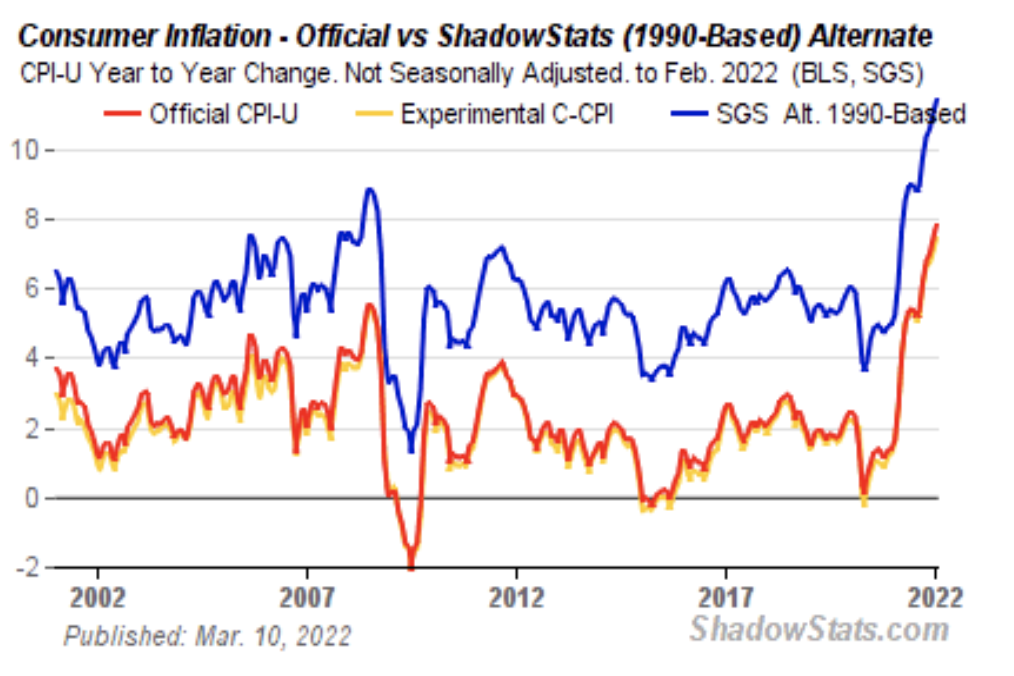

Shadowstats.com still does the CPI analysis with the same format of the formula in 1990 and 1980. This is important because comparing the current CPI formula in 2022 to CPI in 1982, the last time we were at these heightened levels, it doesn't seem as bad.

However the 1982 CPI reading is calculated using the 1980 formula.

If we compare 2022 CPI to 1982 using the 1980 formula on 2022 data, now we are comparing apples to apples, not apples to oranges.

Using the 1980 formula, current CPI is about 17%!!!!

If we compare using the 1990 formula for CPI we are about 12% today.

In order to slow inflation down the Fed can raise rates, which makes the cost of borrowing go up and should slow spending, theoretically.

Would a 25 basis point rise in interest rates really slow spending all that much? I can't see how consumers are going to notice a 25 basis point hike. If the value of your house is up over 20% in one year, or nearly 50% in two years like in the Phoenix metro area, 25 basis points is laughable.

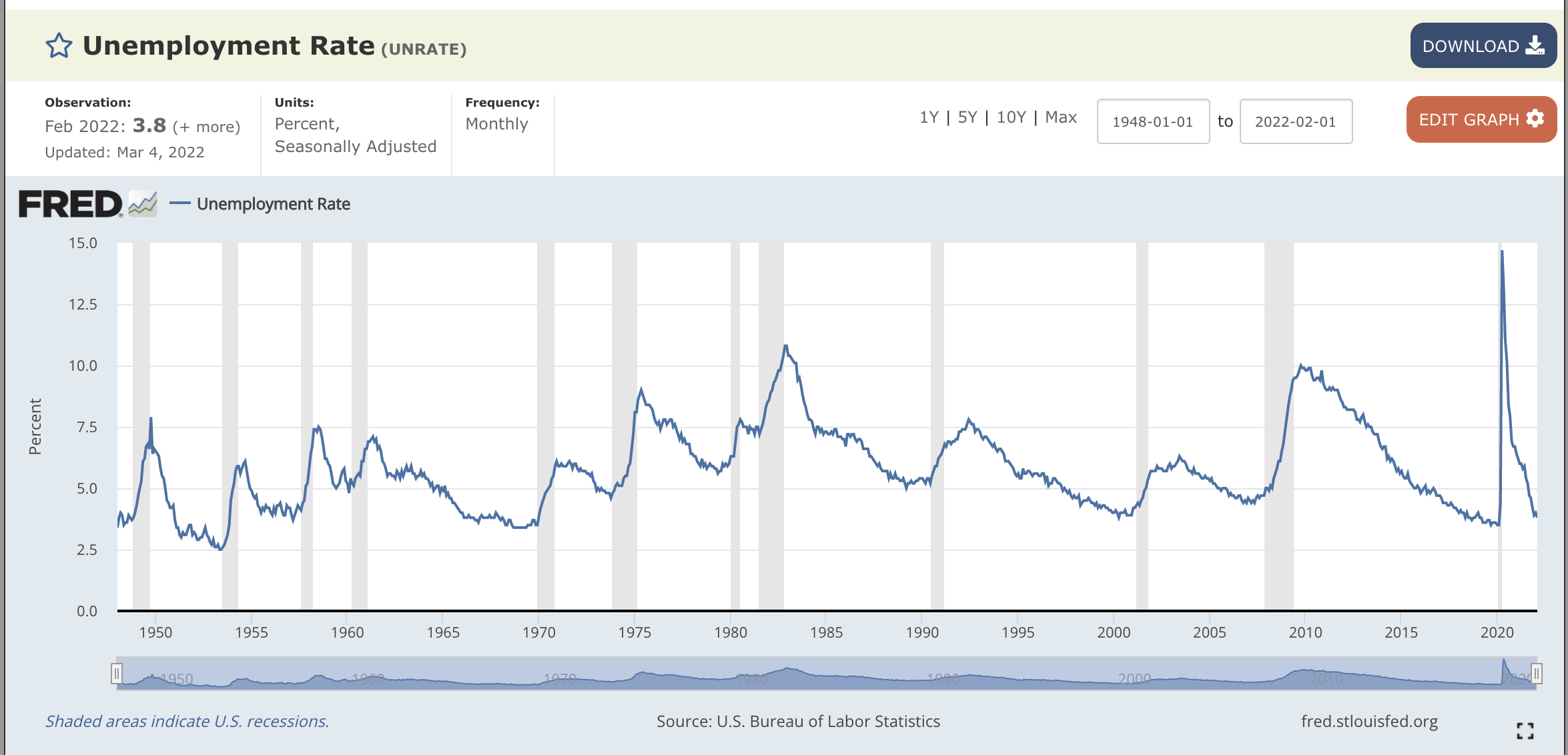

One thing driving inflation is the unemployment rate is nearly as low as it has been since World War 2. (source: https://fred.stlouisfed.org/series/UNRATE)

Notice the vertical lines on the chart. These indicate recessions. What happened right before a recession?

Unemployment was at very low rates.

This isn't a huge surprise, when everyone is employed, consumers buy and buy and buy, feeling quite secure with that steady monthly income.

When rates are low, businesses can borrow at profitable rates to grow faster, which requires hiring more people. More employment means more people are comfortable spending, which drives the prices of goods higher.

AKA Inflation.

The Federal Reserve has three (but really only two) mandates:

What are the goals of monetary policy?

The Federal Reserve Act mandates that the Federal Reserve conduct monetary policy "so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates."1 Even though the act lists three distinct goals of monetary policy, the Fed's mandate for monetary policy is commonly known as the dual mandate. The reason is that an economy in which people who want to work either have a job or are likely to find one fairly quickly and in which the price level (meaning a broad measure of the price of goods and services purchased by consumers) is stable creates the conditions needed for interest rates to settle at moderate levels.2

Maximum Employment = Done

Stable Prices = Definitely Not Done

So how do you slow down price growth, the Fed will look to make it more expensive to borrow, hopefully slowing down inflation.

Ok, the basic Macro Economics discussion is interesting to understand inflation, but let's get in to just how tight the rope we are walking is right now.

Historically speaking, compared back to the 1960's the US Dollar is fairly tame, nothing like the volatility of the 1980's or even near the Dot Com bubble and 9/11. During times of crisis and great fear, the dollar is the safe haven that everyone runs into.

Another safe haven is the Euro, right now the $EURUSD is hitting a historically significant support line. The weakness in the Euro vs the Strength in the US Dollar shows that the Dollar is where scared money is moving, fearing something bigger aka WW3, in Europe.

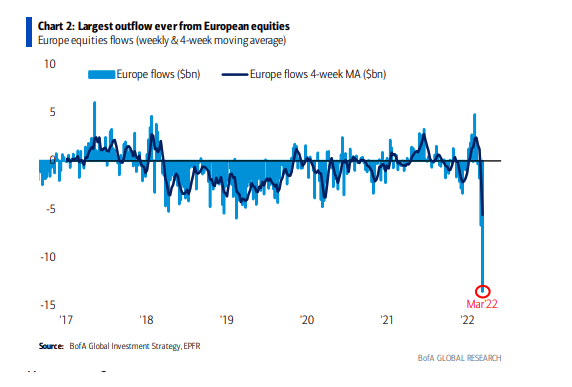

It isn't just the Euro currency itself, but European Equities, look at that mass exodus!

Another currency safe haven is the Japanese Yen. Notice that the wedge formation that is currently holding up on $EURUSD (chart above) has broken to the downside on the $JPYUSD pair already. Do they know something in Japan?

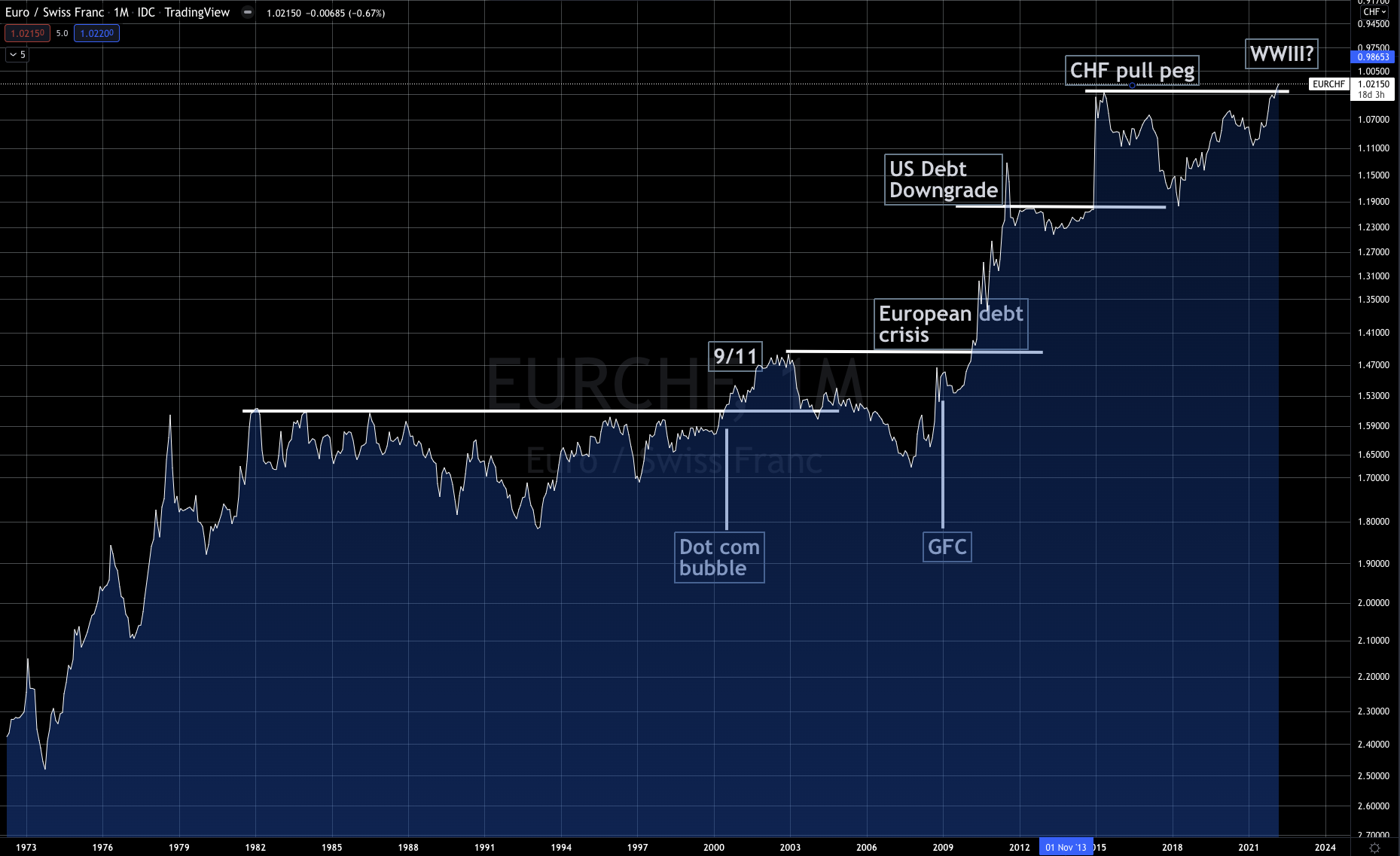

Most importantly the $EURCHF Euro vs Swiss Franc pair is at a historically new level. The Swiss Franc is a major safe haven currency and the $EURCHF level has been breeched, indicating something very big globally has changed.

All of this is happening while the Federal Reserve and most market participants are signaling 7 rate hikes from here.

Unless something changes dramatically, I don't think that'll happen.

Credit markets not equity markets are what forces the Federal Reserve to step in. That is even while equity markets sell off 10-20% from their highs, the Fed hasn't lifted a finger to help. In fact they've done the opposite, they've signaled that they will be raising rates and cutting inflation.

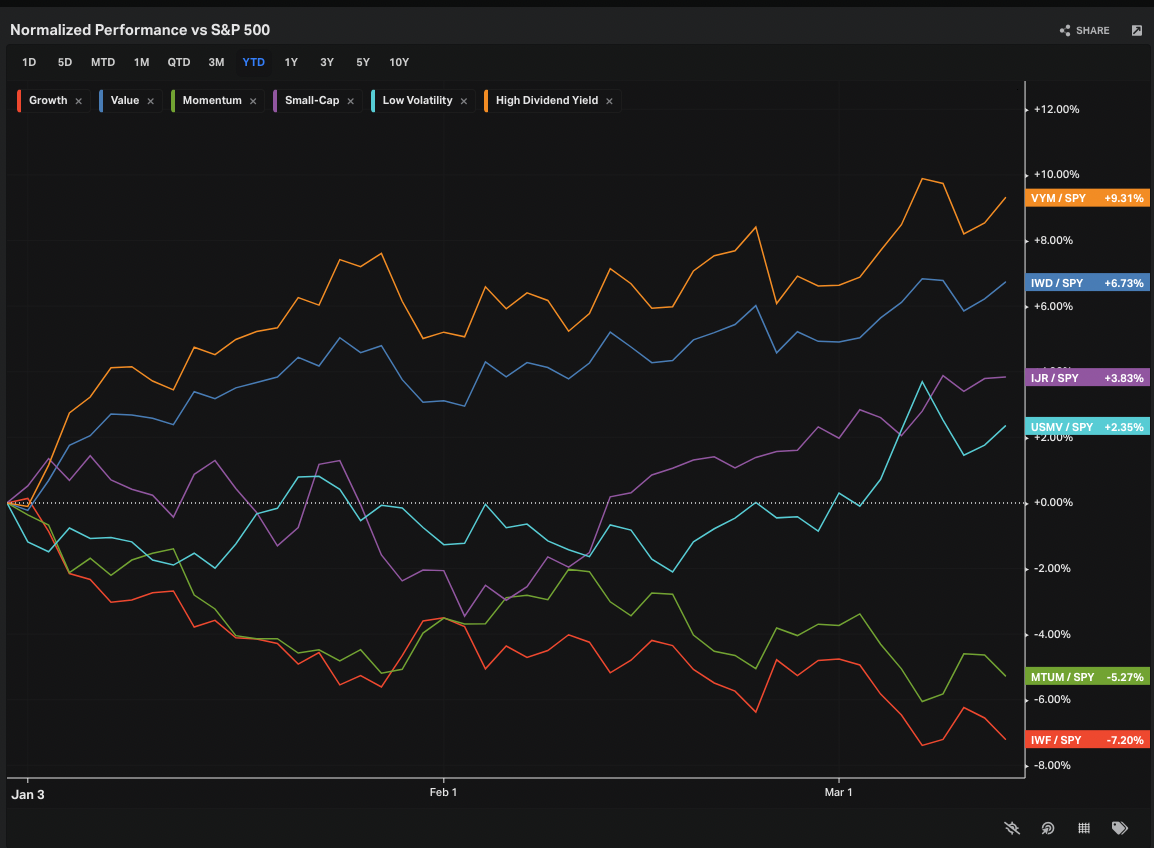

That changes the calculus in high growth, high leverage names, which is why we saw Momentum and Growth take a hit this year, while Value and High Dividend earners benefited the most.

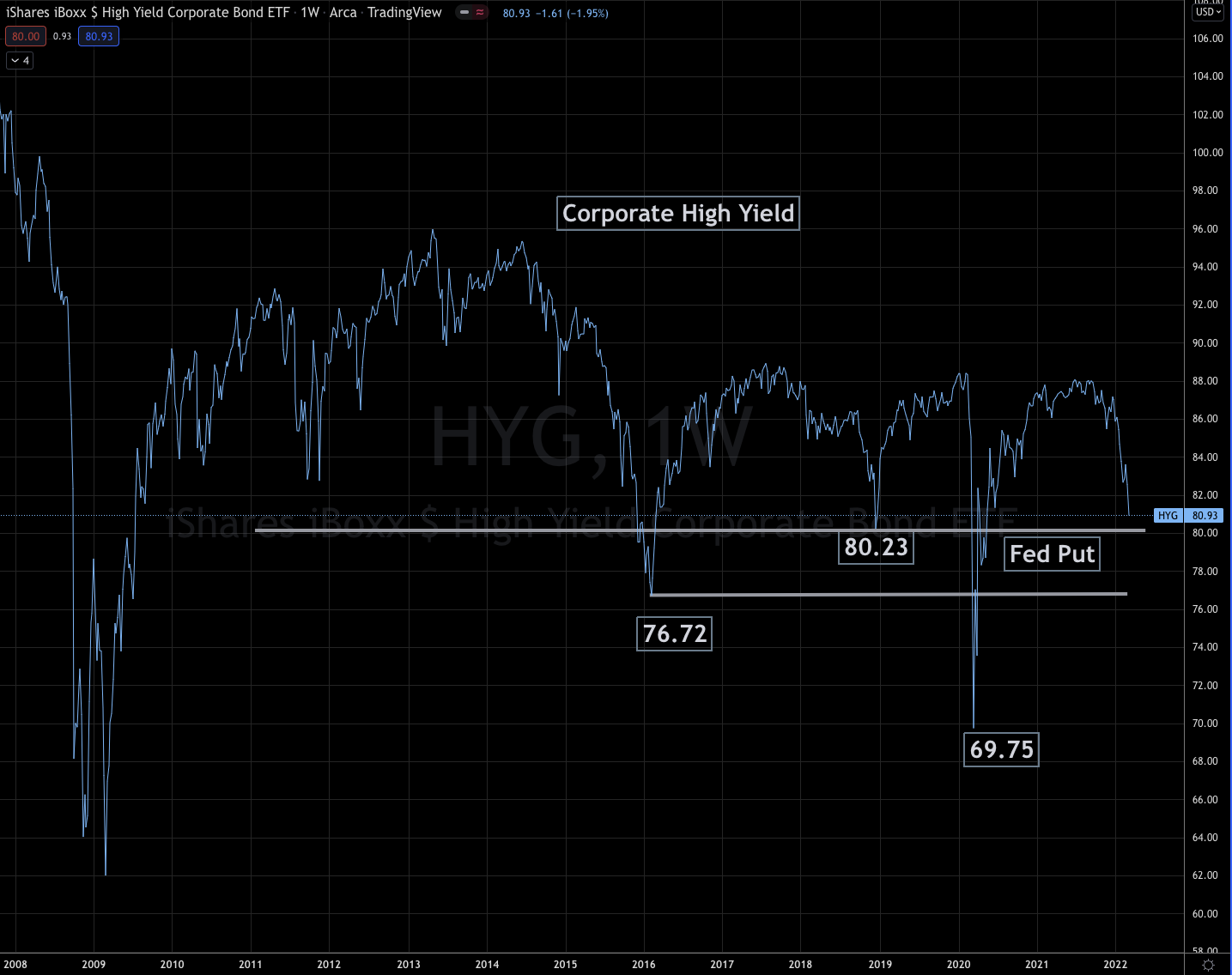

The tripwire that I've been monitoring is the High Yield Credit Markets. The Fed will not let the credit markets get hurt, much past this key level that we are accelerating towards rapidly.

If you recall 2018, a mid-term election year (like this year), the equity markets spent a good chunk of that year selling off. Here's a reminder.

It wasn't until $HYG got to 80.23 that they stepped in. In 2020, Covid moved too far too fast, and so did the Fed.

Since the Global Financial Crisis, the Fed has implemented a number of new techniques, and I bet we can see WHEN they will step in...that's .70 cents lower from here on $HYG.

That's when the magical "Fed Put" will be in play. The question is do they buy the put this time, or do they push things, which could be historically bad.

Let's put all of this together now.

- Nearly historical unemployment.

- Historically low interest rates.

- Historically fast Inflation spike (Rate of Change).

- War in Ukraine with Russia.

- Iran shooting Ballistic missiles into Iraq, a sovereign nation, during the JCPOA (Iran Nuclear deal).

- Equity markets in a correction.

- $EURUSD at historically significant support.

- $USDJPY blowing through that historically significant support.

- $EURCHF at never before seen levels in history.

- Corporate High Yield near crisis level support.

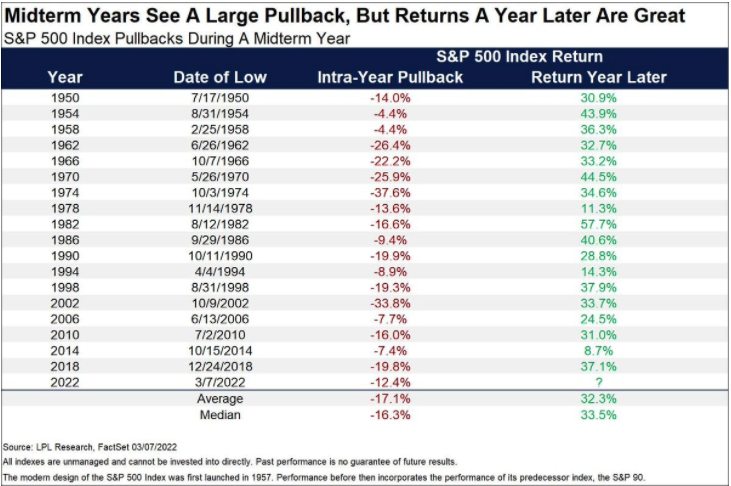

Oh and this little snippet about S&P 500 returns during Midterm election years.

And now, we tap dance our way into the FOMC meeting on Wednesday. This is absolutely a very high risk environment.

I am currently positioned about 70% cash, and have been for most of 2022, with a couple of very small trades on in $SLB, $SPY and $LUNAUSD.

As I wrote about in yesterdays email, this is an environment to either be rotated into what is trending using the Swing Beast Momentum Strategy (energy, commodities, interest rates) or be a day trader.

In the Trading Lab we are taking advantage of these incredible moves throughout the day. It is the ideal environment to be day trading and going to cash at the end of the trading day, and sleeping soundly.

Lab Members get access to the Swing Beast strategy for 1/2 price. (DM me in the lab and I'll get you the link to get your discount).

It's the perfect time to grab this opportunity and sign up for the Trading Lab. We are offering a $200 discount for the first month, this offer ends TOMORROW!

Take this opportunity today and get two of my proven strategy courses FREE!

As a Trading Lab member, you receive...

Daily Livestream - Day trade right alongside me, see what I'm looking at in the markets, work alongside a team of fellow traders.

Daily Morning Brief - each morning I cover what key levels I'm watching, what markets I'm watching that day, and potential trade ideas.

Monthly Macro Trade Strategy - Our long term Global Macro focused ETF end of Month strategy

Swing Trade Alerts - Real-time trade alerts for Options, Futures, Forex, Crypto

Prop Swing Alerts - Designed specifically for Prop Traders who are doing tryouts or managing a live prop account. These are end-of-the-day, swing trades in FX, Commodities, Equities, Metals, Energy, and Interest Rates markets.

Trading Lab Trading Course - I get it, do you pay for a course, or sign up for the Lab? Do both! I created a course for Lab members exclusively, that includes all the different trading strategies, backtesting, trading lessons, techniques, basically a summary of all my courses and everything in The Lab altogether. This alone is valued at $2000 but you get it included in your Lab Membership

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.